The price of houses in the U.S. has risen drastically over the last decade. Homes can fetch as much as 42% more on average than they could only ten years ago. As the cost of living and housing expenses continues to trend upwards, it’s vital to make sure you know exactly what you can afford when buying a home.

How To Set Your Home Buying Budget

The Home Buyers, Inc.

To do this, you have to develop your homebuying budget. Think that’s just determining a mortgage payment? Think again. A homebuying budget needs to consider utilities, HOA fees, commute distance, access to local amenities, and more. Seem like a lot? We understand. That’s why The Home Buyers has determined the key areas to consider when creating your budget.

Contact The Home Buyers to Start Your Home Ownership Journey

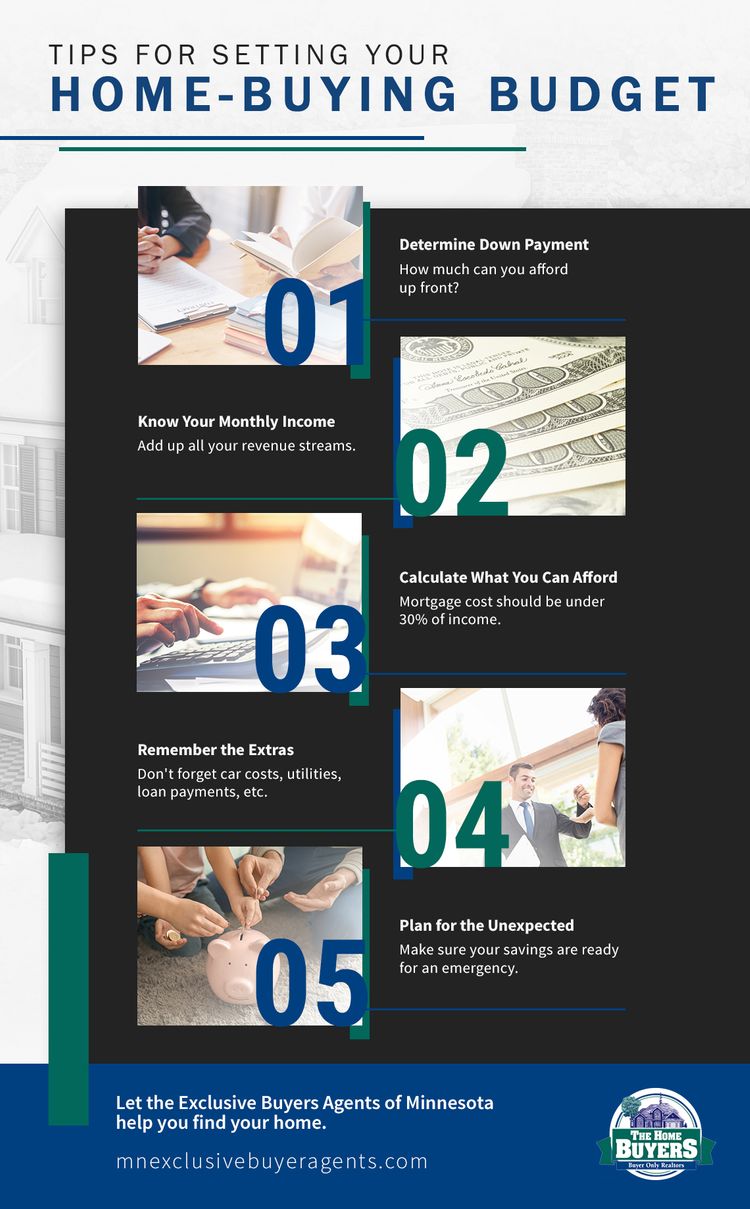

How Much Can You Pay Up Front?

A 20% down payment has been the golden standard in the real estate industry for a while. This high percentage acts as an assurance for mortgage lenders. It used to be the case that lenders would not even entertain the idea of less than 20%. However, paying a 20% downpayment in the modern market is much easier said than done. Imagine buying a house in New York, where the median house list for just under $900k. A 20% down payment means a buyer would need nearly $200,000 in the bank!

Fortunately, as the markets have changed, so too have mortgage lenders. Most now offer down payment options as low as 10%. In rare cases, they’ll even go as low as 3%. However, to protect themselves, mortgage lenders will often require Private Mortgage Insurance, or PMI, with a rate that low. This means paying 20% or more down still has a clear advantage. But, for the typical homebuyer, there are a slew of alternative options available.

How Much Can You Commit To Monthly?

Your starting place here is your pay stub. How much are you bringing in every month? Note that number. You should plan on a monthly mortgage payment that is no more than 30% of your monthly income. Banks tend to favor monthly mortgage payments in this range. But just because you can get approved for a budget that is 30% of your monthly income doesn’t necessarily mean you should.

There is an assortment of other expenses to consider on top of your mortgage payment. Car payments, childcare expenses, eating out, grocery shopping, student debt payments, monthly utilities, savings, and more will soak up that paycheck in a flash. Consider compromising on some luxuries and aiming for a home that will leave you with a lower monthly payment. A house that’s only $10-$20k cheaper could mean the difference between financial security and constant stress.

Do You Have A Plan For Unexpected Expenses?

Homeownership can be liberating, but there are financial risks a homeowner faces that a renter does not. These risks include pipe repairs, electrical work, roof damage, and more that can increase your yearly budget by thousands. These kinds of surprise expenses can easily overwhelm your client.

Make sure you’re ready for the responsibility of a homeowner. You’ll need tools and equipment to maintain the house and property. You’ll be responsible for things as small as lightbulb repairs to as expensive as furnace replacements. You need to have a healthy amount of savings built up to account for these unforeseen expenses.

Buying a home is a process that should be approached with extreme care. Make sure you do your research and spend plenty of time building that well-thought-out budget. Then, once you’ve found a home you love and can comfortably afford, buy it! You’ll experience what it means to own, not rent, a house!

Are you ready to take the next step towards homeownership, but still aren’t exactly sure where to start? The Home Buyers can help. Contact us to speak to one of our expert buyer’s agents today!